Raumbeispiel

111

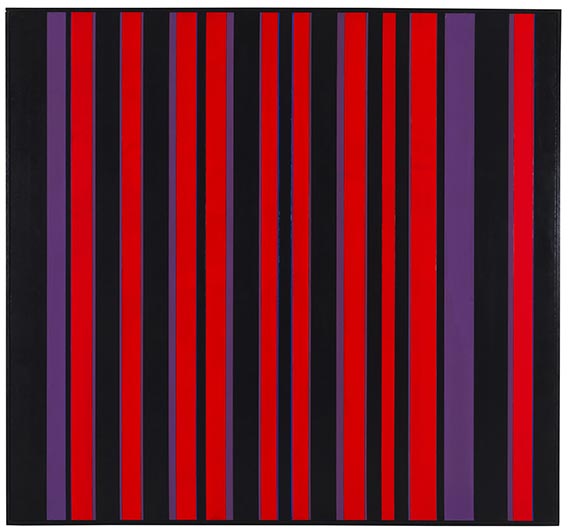

Günter Fruhtrunk

Übergang zur Selbstbewegung, 1957.

Oil and mixed media on canvas, on panel

Estimate:

€ 20,000 - 30,000

$ 21,400 - 32,100

Übergang zur Selbstbewegung. 1957.

Oil and mixed media on canvas, on panel.

Signed, monogrammed, dated and inscribed on the reverse. Stretcher titled and inscribed with a direction arrow. 65 x 92 cm (25.5 x 36.2 in).

[SM].

• Lately featuring in the acclaimed show "Günter Fruhtrunk. Die Pariser Jahre (1954-1967)" at the Lenbachhaus, Munich, November 21, 2023 - April 7, 2024.

• Early work from the Paris period.

• Günter Fruhtrunk gave Constructivism its own dynamic form through a consistent reorientation.

PROVENANCE: Private collection Southern Germany.

EXHIBITION: 50 ans de peinture abstraite. Exposition internationale organisée à la ocassion de la publication du Dictionnaire de la peinture abstraite, Galerie Ceuze, Paris, May 9 - JUne 12, 1957, no. 131.

Günter Fruhtrunk, Museum am Ostwall, Dortmund, November 1963.

LITERATURE: Silke Reiter, Günter Fruhtrunk. Werkverzeichnis der Bilder, 1952-1982, 2018, no. 110.

--

Sturies Auktionen, Düsseldorf, November 10, 2007, lot 54.

Called up: June 7, 2024 - ca. 13.46 h +/- 20 min.

Oil and mixed media on canvas, on panel.

Signed, monogrammed, dated and inscribed on the reverse. Stretcher titled and inscribed with a direction arrow. 65 x 92 cm (25.5 x 36.2 in).

[SM].

• Lately featuring in the acclaimed show "Günter Fruhtrunk. Die Pariser Jahre (1954-1967)" at the Lenbachhaus, Munich, November 21, 2023 - April 7, 2024.

• Early work from the Paris period.

• Günter Fruhtrunk gave Constructivism its own dynamic form through a consistent reorientation.

PROVENANCE: Private collection Southern Germany.

EXHIBITION: 50 ans de peinture abstraite. Exposition internationale organisée à la ocassion de la publication du Dictionnaire de la peinture abstraite, Galerie Ceuze, Paris, May 9 - JUne 12, 1957, no. 131.

Günter Fruhtrunk, Museum am Ostwall, Dortmund, November 1963.

LITERATURE: Silke Reiter, Günter Fruhtrunk. Werkverzeichnis der Bilder, 1952-1982, 2018, no. 110.

--

Sturies Auktionen, Düsseldorf, November 10, 2007, lot 54.

Called up: June 7, 2024 - ca. 13.46 h +/- 20 min.

111

Günter Fruhtrunk

Übergang zur Selbstbewegung, 1957.

Oil and mixed media on canvas, on panel

Estimate:

€ 20,000 - 30,000

$ 21,400 - 32,100

Buyer's premium, taxation and resale right compensation for Günter Fruhtrunk "Übergang zur Selbstbewegung"

This lot can be purchased subject to differential or regular taxation, artist‘s resale right compensation is due.

Differential taxation:

Hammer price up to 800,000 €: herefrom 32 % premium.

The share of the hammer price exceeding 800,000 € is subject to a premium of 27 % and is added to the premium of the share of the hammer price up to 800,000 €.

The share of the hammer price exceeding 4,000,000 € is subject to a premium of 22 % and is added to the premium of the share of the hammer price up to 4,000,000 €.

The buyer's premium contains VAT, however, it is not shown.

Regular taxation:

Hammer price up to 800,000 €: herefrom 27 % premium.

The share of the hammer price exceeding 800,000 € is subject to a premium of 21% and is added to the premium of the share of the hammer price up to 800,000 €.

The share of the hammer price exceeding 4,000,000 € is subject to a premium of 15% and is added to the premium of the share of the hammer price up to 4,000,000 €.

The statutory VAT of currently 19 % is levied to the sum of hammer price and premium. As an exception, the reduced VAT of 7 % is added for printed books.

We kindly ask you to notify us before invoicing if you wish to be subject to regular taxation.

Calculation of artist‘s resale right compensation:

For works by living artists, or by artists who died less than 70 years ago, a artist‘s resale right compensation is levied in accordance with Section 26 UrhG:

4 % of hammer price from 400.00 euros up to 50,000 euros,

another 3 % of the hammer price from 50,000.01 to 200,000 euros,

another 1 % for the part of the sales proceeds from 200,000.01 to 350,000 euros,

another 0.5 % for the part of the sale proceeds from 350,000.01 to 500,000 euros and

another 0.25 % of the hammer price over 500,000 euros.

The maximum total of the resale right fee is EUR 12,500.

The artist‘s resale right compensation is VAT-exempt.

Differential taxation:

Hammer price up to 800,000 €: herefrom 32 % premium.

The share of the hammer price exceeding 800,000 € is subject to a premium of 27 % and is added to the premium of the share of the hammer price up to 800,000 €.

The share of the hammer price exceeding 4,000,000 € is subject to a premium of 22 % and is added to the premium of the share of the hammer price up to 4,000,000 €.

The buyer's premium contains VAT, however, it is not shown.

Regular taxation:

Hammer price up to 800,000 €: herefrom 27 % premium.

The share of the hammer price exceeding 800,000 € is subject to a premium of 21% and is added to the premium of the share of the hammer price up to 800,000 €.

The share of the hammer price exceeding 4,000,000 € is subject to a premium of 15% and is added to the premium of the share of the hammer price up to 4,000,000 €.

The statutory VAT of currently 19 % is levied to the sum of hammer price and premium. As an exception, the reduced VAT of 7 % is added for printed books.

We kindly ask you to notify us before invoicing if you wish to be subject to regular taxation.

Calculation of artist‘s resale right compensation:

For works by living artists, or by artists who died less than 70 years ago, a artist‘s resale right compensation is levied in accordance with Section 26 UrhG:

4 % of hammer price from 400.00 euros up to 50,000 euros,

another 3 % of the hammer price from 50,000.01 to 200,000 euros,

another 1 % for the part of the sales proceeds from 200,000.01 to 350,000 euros,

another 0.5 % for the part of the sale proceeds from 350,000.01 to 500,000 euros and

another 0.25 % of the hammer price over 500,000 euros.

The maximum total of the resale right fee is EUR 12,500.

The artist‘s resale right compensation is VAT-exempt.