Raumbeispiel

107

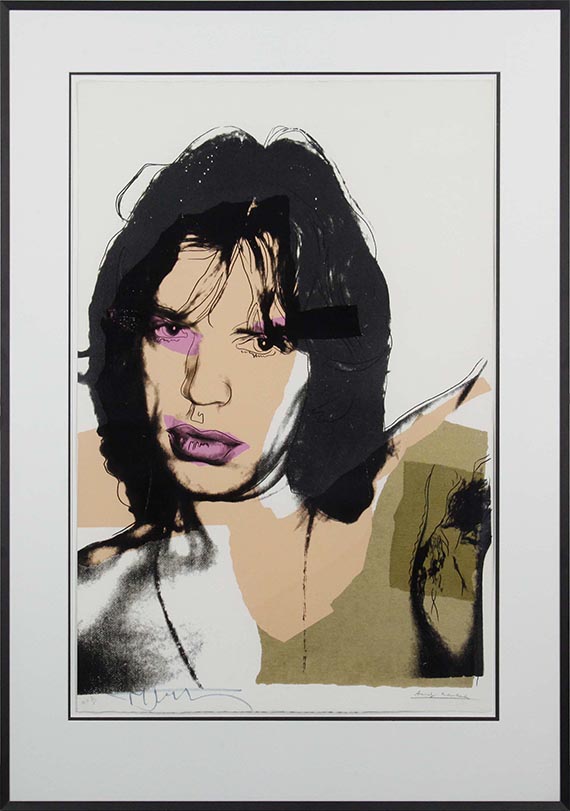

Andy Warhol

Mick Jagger, 1975.

Silkscreen in colors

Estimate:

€ 70,000 / $ 79,800 Sold:

€ 122,550 / $ 139,707 (incl. surcharge)

107

Andy Warhol

Mick Jagger, 1975.

Silkscreen in colors

Estimate:

€ 70,000 / $ 79,800 Sold:

€ 122,550 / $ 139,707 (incl. surcharge)

Andy Warhol

1928 - 1987

Mick Jagger. 1975.

Silkscreen in colors.

Signed and numbered, as well as signed by Mick Jagger. One of 50 artist proofs aside from the edition of 250 copies. On structured Arches paper (no watermark). 99 x 73.5 cm (38.9 x 28.9 in). Sheet: 111 x 73,5 cm (43,7 x 28,9 in).

Printed by Alexander Heinrici, New York. Published b Seabird Editions, London (with the copyright stamp on the reverse). [EH].

• The portrait of “Mick Jagger” is one of Andy Warhol’s most iconic works.

• In the same year the portrait was made, Andy Warhol incorporated voluminous color fields and lines into his silkscreen prints.

• Warhol’s enormous oeuvre includes paintings and silkscreen prints that all have one thing in common: repetitive motifs with a high recognition and flat surfaces.

PROVENANCE: Private collection, Baden-Württemberg.

LITERATURE: Frayda Feldman, Jörg Schellmann, Claudia Defendi. Andy Warhol Prints. A catalogue raisonné 1962-1987, New York 2003, CR no. II 141.

1928 - 1987

Mick Jagger. 1975.

Silkscreen in colors.

Signed and numbered, as well as signed by Mick Jagger. One of 50 artist proofs aside from the edition of 250 copies. On structured Arches paper (no watermark). 99 x 73.5 cm (38.9 x 28.9 in). Sheet: 111 x 73,5 cm (43,7 x 28,9 in).

Printed by Alexander Heinrici, New York. Published b Seabird Editions, London (with the copyright stamp on the reverse). [EH].

• The portrait of “Mick Jagger” is one of Andy Warhol’s most iconic works.

• In the same year the portrait was made, Andy Warhol incorporated voluminous color fields and lines into his silkscreen prints.

• Warhol’s enormous oeuvre includes paintings and silkscreen prints that all have one thing in common: repetitive motifs with a high recognition and flat surfaces.

PROVENANCE: Private collection, Baden-Württemberg.

LITERATURE: Frayda Feldman, Jörg Schellmann, Claudia Defendi. Andy Warhol Prints. A catalogue raisonné 1962-1987, New York 2003, CR no. II 141.

In the spring of 1975, the Rolling Stones rented Warhol’s Montauk Church Estate on Long Island to prepare for their upcoming tour. Warhol used this opportunity to take numerous photographs of Mick Jagger, depicting him bare-chested in various poses. By using his own snapshots for the resulting graphic portraits, Warhol eliminates a defining element of his earlier work. He made portfolios of ten different portraits, for which he used a new technique: a combination of photography, collage, and drawn lines. Like strips of paper, he laid areas of color over the actual image, creating striking, flirtatious depictions of the musician. Alongside the Marilyn Monroe series, the mid-1970s portraits of Mick Jagger rank among Andy Warhol’s most famous. The frontman of the Rolling Stones, a band founded in 1962 that had already completed numerous tours across America and Europe by then and achieved worldwide fame not only through their progressive music but also through their provocative stage shows, was virtually regarded as a symbol of freedom that defied all social conventions. The eccentric Warhol, who had found his own trademark look in the 1960s with a white-blond wig and black sunglasses, must have recognized in Mick Jagger an eccentric alter ego that inspired him to create these landmark portraits. A distinctive feature is the musician’s signature on some of the prints. Not only the “painter” but also his model immortalize themselves in these works. [EH]

Headquarters

Joseph-Wild-Str. 18

81829 Munich

Phone: +49 89 55 244-0

Fax: +49 89 55 244-177

info@kettererkunst.de

Louisa von Saucken / Undine Schleifer

Holstenwall 5

20355 Hamburg

Phone: +49 40 37 49 61-0

Fax: +49 40 37 49 61-66

infohamburg@kettererkunst.de

Dr. Simone Wiechers / Nane Schlage

Fasanenstr. 70

10719 Berlin

Phone: +49 30 88 67 53-63

Fax: +49 30 88 67 56-43

infoberlin@kettererkunst.de

Cordula Lichtenberg

Gertrudenstraße 24-28

50667 Cologne

Phone: +49 221 510 908-15

infokoeln@kettererkunst.de

Hessen

Rhineland-Palatinate

Miriam Heß

Phone: +49 62 21 58 80-038

Fax: +49 62 21 58 80-595

infoheidelberg@kettererkunst.de

We will inform you in time.