Frame image

Raumbeispiel

247

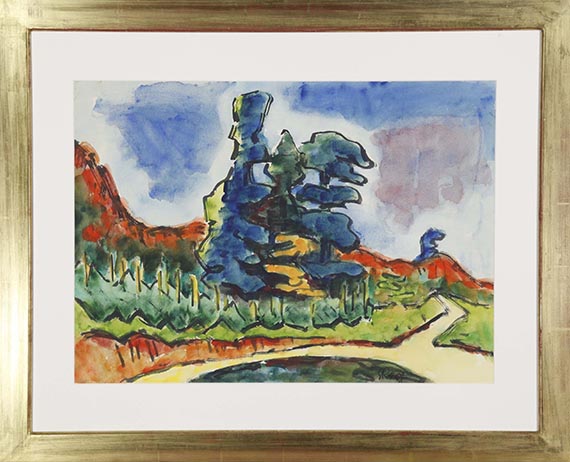

Karl Schmidt-Rottluff

Waldrand am Taunus, 1963.

Watercolor

Estimate:

€ 20,000 / $ 23,600 Sold:

€ 43,180 / $ 50,952 (incl. surcharge)

Waldrand am Taunus. 1963.

Watercolor.

Signed lower right. Stamped lower left with the work number “6345”. Titled on the reverse. On wove paper. 50.2 x 70.5 cm (19.7 x 27.7 in), the full sheet.

[MH].

• Particularly vibrant and expressive landscape depiction with a pictorial effect.

• Impressive visualization of his artistic principle: the combination of line and autonomous forms as an aesthetic ideal.

• The great Expressionist rendered the composition with bold contours, a contrasting palette and dynamic ease.

The watercolor is documented in the archive of the Karl and Emy Schmidt-Rottluff Foundation.

PROVENANCE: Private collection, Bavaria.

Private collection, Lower Saxony (since 1996, gifted from the above).

Private collection, Rhineland-Palatinate (since 2018, inherited from the above).

Watercolor.

Signed lower right. Stamped lower left with the work number “6345”. Titled on the reverse. On wove paper. 50.2 x 70.5 cm (19.7 x 27.7 in), the full sheet.

[MH].

• Particularly vibrant and expressive landscape depiction with a pictorial effect.

• Impressive visualization of his artistic principle: the combination of line and autonomous forms as an aesthetic ideal.

• The great Expressionist rendered the composition with bold contours, a contrasting palette and dynamic ease.

The watercolor is documented in the archive of the Karl and Emy Schmidt-Rottluff Foundation.

PROVENANCE: Private collection, Bavaria.

Private collection, Lower Saxony (since 1996, gifted from the above).

Private collection, Rhineland-Palatinate (since 2018, inherited from the above).

247

Karl Schmidt-Rottluff

Waldrand am Taunus, 1963.

Watercolor

Estimate:

€ 20,000 / $ 23,600 Sold:

€ 43,180 / $ 50,952 (incl. surcharge)

Headquarters

Joseph-Wild-Str. 18

81829 Munich

Phone: +49 89 55 244-0

Fax: +49 89 55 244-177

info@kettererkunst.de

Louisa von Saucken / Undine Schleifer

Holstenwall 5

20355 Hamburg

Phone: +49 40 37 49 61-0

Fax: +49 40 37 49 61-66

infohamburg@kettererkunst.de

Dr. Simone Wiechers / Nane Schlage

Fasanenstr. 70

10719 Berlin

Phone: +49 30 88 67 53-63

Fax: +49 30 88 67 56-43

infoberlin@kettererkunst.de

Cordula Lichtenberg

Gertrudenstraße 24-28

50667 Cologne

Phone: +49 221 510 908-15

infokoeln@kettererkunst.de

Hessen

Rhineland-Palatinate

Miriam Heß

Phone: +49 62 21 58 80-038

Fax: +49 62 21 58 80-595

infoheidelberg@kettererkunst.de

We will inform you in time.