Frame image

351

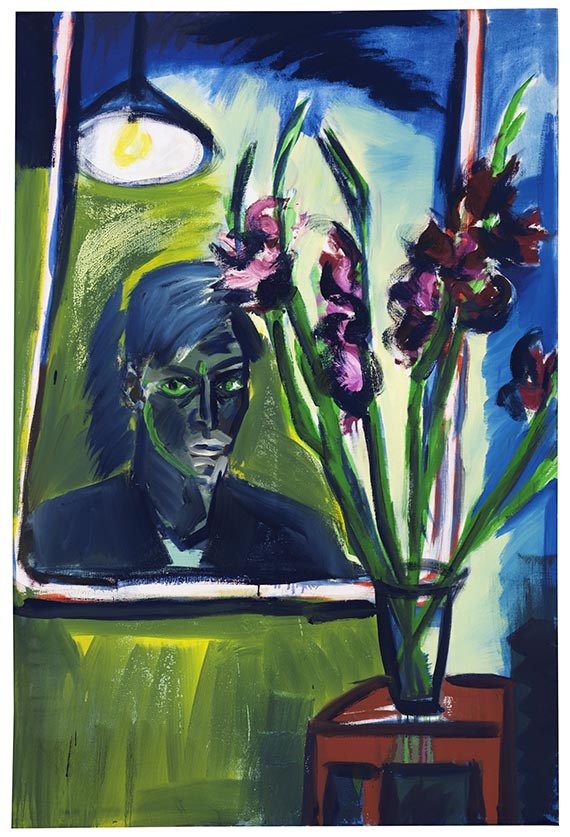

Rainer Fetting

Selbstportrait mit Blumen III, 1981.

Oil on canvas

Estimate:

€ 50,000 / $ 59,000 Sold:

€ 76,200 / $ 89,916 (incl. surcharge)

Selbstportrait mit Blumen III. 1981.

Oil on canvas.

Signed, dated and titled on the reverse of the canvas. 200 x 135 cm (78.7 x 53.1 in). [AW].

• By combining two classic genres, Rainer Fetting created an expressive reinterpretation that is typical of his art.

• Fetting's clear formal division of the pictorial surface and the dramatic accentuation create an enormous expressiveness.

• A protagonist of the “Neue Wilden” (New Wild Artists).

• The paintings from the early 1980s are among his most sought-after works.

• Other works from the 1980s are included in the collections of the Tate Gallery, London, the Städel Museum, Frankfurt am Main, and the Pinakothek der Moderne, Munich.

The artist confirmed the authenticity of the present work. The work bears the work number "D/25". We are grateful for the kind support in cataloging this lot.

PROVENANCE: Galerie Karl Pfefferle, Munich (with the gallery label on the stretcher).

Private collection, Hamburg (acquired from the above in 2004).

"Throughout the decades, I repeatedly painted flower pictures – deliberately and with particular pleasure, especially when the prevailing zeitgeist completely frowned upon them, that is, during the so-called 'wild painters' period. In a gray Berlin winter in the old walled city, it was a feast for the eyes to put together a magnificent flower bouquet. It is often ignored that not all 'flower paintings' are the same. It is always important to see them in context and how they were made."

Rainer Fetting in March 2020.

Oil on canvas.

Signed, dated and titled on the reverse of the canvas. 200 x 135 cm (78.7 x 53.1 in). [AW].

• By combining two classic genres, Rainer Fetting created an expressive reinterpretation that is typical of his art.

• Fetting's clear formal division of the pictorial surface and the dramatic accentuation create an enormous expressiveness.

• A protagonist of the “Neue Wilden” (New Wild Artists).

• The paintings from the early 1980s are among his most sought-after works.

• Other works from the 1980s are included in the collections of the Tate Gallery, London, the Städel Museum, Frankfurt am Main, and the Pinakothek der Moderne, Munich.

The artist confirmed the authenticity of the present work. The work bears the work number "D/25". We are grateful for the kind support in cataloging this lot.

PROVENANCE: Galerie Karl Pfefferle, Munich (with the gallery label on the stretcher).

Private collection, Hamburg (acquired from the above in 2004).

"Throughout the decades, I repeatedly painted flower pictures – deliberately and with particular pleasure, especially when the prevailing zeitgeist completely frowned upon them, that is, during the so-called 'wild painters' period. In a gray Berlin winter in the old walled city, it was a feast for the eyes to put together a magnificent flower bouquet. It is often ignored that not all 'flower paintings' are the same. It is always important to see them in context and how they were made."

Rainer Fetting in March 2020.

351

Rainer Fetting

Selbstportrait mit Blumen III, 1981.

Oil on canvas

Estimate:

€ 50,000 / $ 59,000 Sold:

€ 76,200 / $ 89,916 (incl. surcharge)

Headquarters

Joseph-Wild-Str. 18

81829 Munich

Phone: +49 89 55 244-0

Fax: +49 89 55 244-177

info@kettererkunst.de

Louisa von Saucken / Undine Schleifer

Holstenwall 5

20355 Hamburg

Phone: +49 40 37 49 61-0

Fax: +49 40 37 49 61-66

infohamburg@kettererkunst.de

Dr. Simone Wiechers / Nane Schlage

Fasanenstr. 70

10719 Berlin

Phone: +49 30 88 67 53-63

Fax: +49 30 88 67 56-43

infoberlin@kettererkunst.de

Cordula Lichtenberg

Gertrudenstraße 24-28

50667 Cologne

Phone: +49 221 510 908-15

infokoeln@kettererkunst.de

Hessen

Rhineland-Palatinate

Miriam Heß

Phone: +49 62 21 58 80-038

Fax: +49 62 21 58 80-595

infoheidelberg@kettererkunst.de

We will inform you in time.